Types of Fintech Explained: A Complete Guide to Every Category in the Industry

Explore every major type of fintech in this complete guide. Learn how digital payments, neo banks, lending apps, blockchain, and AI-driven finance are transforming the financial industry in 2026.

Most people use fintech every day without realizing it. They tap their phone to pay, apply for credit online, buy stocks through an app, or get insured without speaking to a single human. What they often do not realize is that these experiences come from completely different categories of fintech, each built on different technology, serving different needs, and operating under different business models.

Understanding the types of fintech matters because it helps you make smarter decisions about which platforms to trust, which services are regulated, and how the digital finance world actually fits together. This guide clearly covers every major fintech category, with real examples and practical context.

What is Fintech and Why Does it Come in Different Types?

Fintech stands for financial technology. It describes any company that uses software, apps, data systems, or automation to deliver financial services. Banks have always used technology, but fintech companies build around it as their core product rather than as a support system.

The reason fintech splits into distinct categories is straightforward: financial services cover an enormous range of human needs.

Paying for groceries, borrowing money to start a business, insuring a car, building a retirement fund, and verifying a customer identity are all financial activities. But each one requires different technology, different regulation, and a different kind of expertise.

Fintech companies specialize. A lending platform focuses entirely on credit assessment and loan distribution. A payment company builds infrastructure for moving money. A wealthtech platform builds tools for investment management. Each category solves a specific financial problem that traditional institutions handled slowly, expensively, or not at all.

Why this matters to you as a user

Different fintech types carry different levels of risk and regulation

Understanding which category a platform belongs to helps you assess how it handles your money

Some fintech types are highly regulated and protected. Others are newer and carry more user risk

Knowing the categories helps you build a smarter personal finance stack rather than downloading apps at random

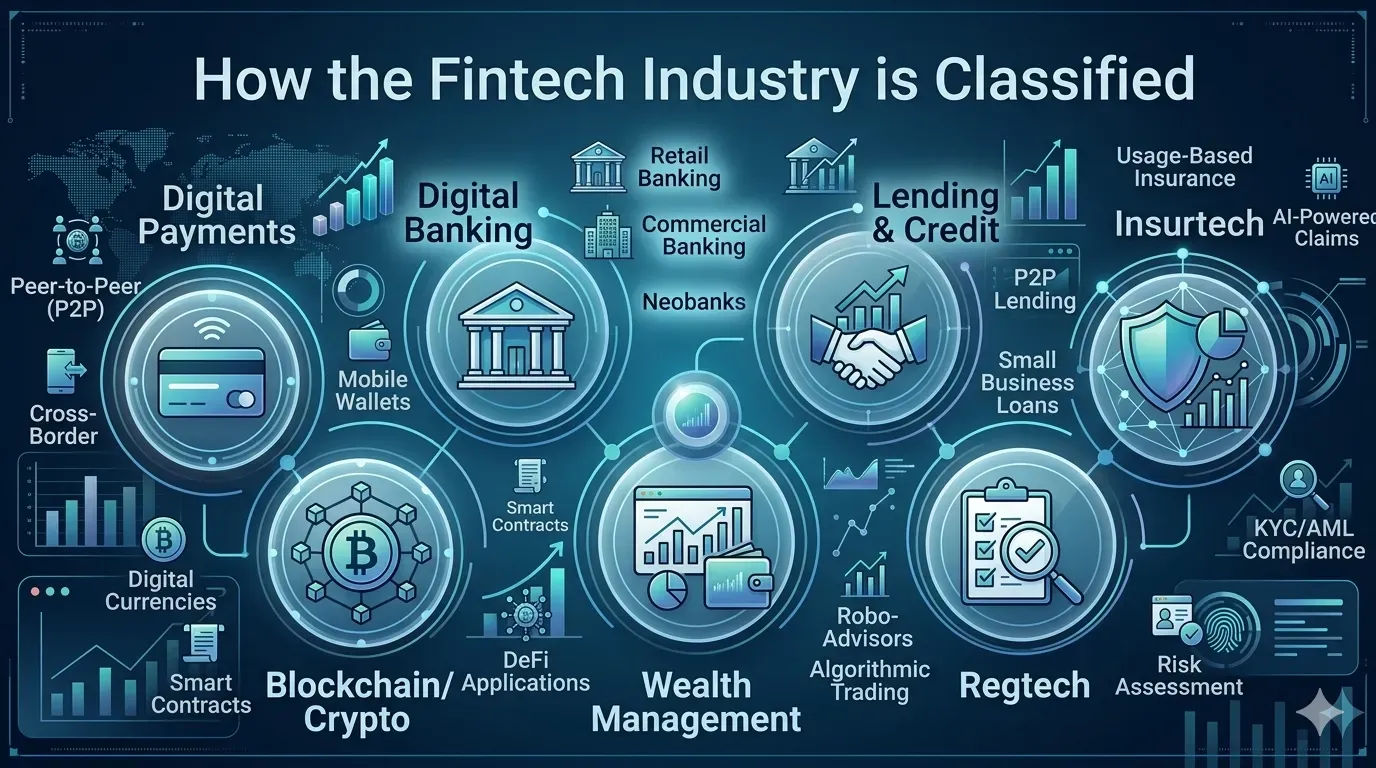

How the Fintech Industry is Classified

Industry analysts, regulators, and investors classify fintech companies based on the financial service they provide and the customer segment they serve. The classification is not perfectly rigid. Many companies operate across more than one category. But the core segments are widely agreed upon and help make sense of a complex industry.

The primary classification logic looks at three questions: What financial problem does the company solve? Who is the customer? And what underlying technology makes the service work?

Classification factor | What it means | Example |

|---|---|---|

Financial service provided | What the platform does with money | Moving it, lending it, investing it, insuring it |

Customer segment | Who uses the platform | Consumers, small businesses, enterprises, institutions |

Core technology | What makes the service work at the back end | APIs, AI models, blockchain, cloud systems |

Regulatory category | Which rules must the platform follow | Banking license, payment processor, securities license |

The 7 Main Types of Fintech: A Complete Breakdown

Here is a clear explanation of every major fintech category, what it does, how it works, and real-world examples of each.

1. Payment Fintech Moving money faster, cheaper, and from anywhere Payment fintech covers every technology that moves money between people, businesses, and accounts. This is the largest and most widely used fintech category. It includes the tap-to-pay on your phone, the checkout button on an e-commerce site, the international transfer app, and the point-of-sale system at a small business.

|

2. Lending Fintech Credit decisions in minutes, not weeks Lending fintech platforms use AI and alternative data to assess creditworthiness and approve loans far faster than traditional banks. They serve individuals who need personal loans, small businesses that need working capital, students refinancing debt, and consumers using installment payment options at checkout.

|

3. WealthTech Investment management for everyone, not just the wealthy WealthTech platforms make investing accessible to people who previously could not afford a financial advisor or meet minimum balance requirements. They range from commission-free stock trading apps to AI-powered robo-advisors that build and manage entire portfolios automatically based on a user's goals and risk tolerance.

|

4. InsurTech Insurance that moves at the speed of real life InsurTech applies technology to the insurance industry, which has historically been slow, paper-heavy, and opaque in its pricing. Digital insurance platforms use AI, real-time data, and behavioral analytics to offer fairer pricing, faster claims processing, and flexible coverage options that traditional insurers cannot match.

|

5. RegTech Compliance automation for regulated industries RegTech, short for regulatory technology, helps financial institutions and businesses manage compliance requirements automatically. Know Your Customer verification, anti-money laundering monitoring, fraud detection, and regulatory reporting are all areas where RegTech tools replace slow, expensive manual processes with automated systems.

|

6. Blockchain Fintech Decentralized finance built on transparent, programmable systems Blockchain fintech covers platforms built on distributed ledger technology. This includes cryptocurrency exchanges, decentralized finance protocols, NFT marketplaces, and cross-border payment systems that use blockchain rails to move money without traditional banking intermediaries. It is the most technically complex and least regulated category.

|

7. Neobanks and Digital Banks Full banking services with no branches and no legacy systems Neobanks are fully digital banks that operate entirely through apps and websites without any physical branches. They offer the core services of a traditional bank, including current accounts, savings accounts, debit cards, and payments, but build everything on modern technology that traditional banks cannot easily replicate. Many offer higher savings rates, lower fees, and a significantly better user experience.

|

Why Different Types of Fintech Exist

The diversity of fintech categories is not arbitrary. Each one emerged because a specific financial need was being served poorly by existing institutions.

Different customers need different solutions

A freelancer managing irregular income needs different tools than a retiree building a fixed-income portfolio. A startup seeking growth capital has different needs than a consumer wanting to split a restaurant bill. Fintech categories exist because financial needs are genuinely diverse, and specialized platforms serve each segment better than generalist institutions can.

Technology enables specialization at scale

Traditional banks needed branches, staff, and physical infrastructure to serve customers. That made it expensive to specialize. A fintech company can build a platform that does one financial task extremely well and scale it globally through software. Specialization became economically viable when technology removed the physical constraints.

Regulation created separate lanes

Different financial services require different regulatory licenses. A company that moves money needs a payment processor license. A company that takes deposits needs a banking license. A company that sells investment products needs securities authorization. These regulatory requirements naturally separate the industry into distinct categories with different rules and protections.

How Fintech Companies Work by Category

Each fintech type has a distinct operating model. Here is a clear breakdown of how each category generates value and revenue.

Fintech Type | How users interact | How the company earns revenue |

|---|---|---|

Payment Fintech | Send, receive, and process payments through apps or APIs | Transaction fees, currency conversion margins, and merchant fees |

Lending Fintech | Apply for loans, receive funds, and repay over time | Interest on loans, origination fees, and late payment charges |

WealthTech | Open accounts, invest, track portfolio performance | Management fees, premium subscriptions, payment for order flow |

InsurTech | Get quoted, buy coverage, file claims through apps | Insurance premiums, referral fees, and data analytics services |

RegTech | Integrate compliance tools via API into existing systems | SaaS subscription fees, per-check transaction fees |

Blockchain Fintech | Buy assets, trade, lend, and borrow on decentralized platforms | Trading fees, spread on transactions, and protocol revenue |

Neobanks | Open accounts, spend, save, and transfer through apps | Interchange fees, premium account subscriptions, and loan products |

Why Fintech Categories Matter: The Benefits for Users

Better financial access for more people

Each fintech category extends financial services to people who previously could not access them. Lending fintech serves customers that traditional banks reject. WealthTech removes the wealth barrier to investing. Neobanks offer accounts to people without a credit history. RegTech makes compliance affordable for small businesses. Collectively, fintech categories make finance more inclusive.

Faster service across every financial activity

Traditional financial institutions take days to process loan applications, weeks to open accounts, and hours to settle international transfers. Fintech companies in every category have reduced these timelines to minutes or seconds. The speed improvement is not marginal. It is structural.

Lower costs at every level

By removing physical branches, manual processes, and legacy systems, fintech companies in every category operate at significantly lower cost than traditional institutions. Those savings translate to lower fees for consumers, better exchange rates on transfers, lower insurance premiums based on actual risk, and free investment accounts that were previously only available to high-net-worth clients.

Digital convenience that matches how people actually live

From a practical perspective, fintech categories exist because people manage their financial lives on their phones, at all hours, from anywhere. Traditional institutions were built for in-person, business-hours interactions. Each fintech category rebuilds a piece of financial infrastructure around the assumption that users want immediate, mobile, self-service access to every financial product they need.

How Users Interact With Multiple Fintech Types Together

The most financially sophisticated users today do not rely on a single institution for all their needs. They build a personal finance stack that draws on multiple fintech categories, each handling a specific job.

A practical daily fintech usage example

Morning: Check your neobank account for overnight balance updates and any unusual transactions. Your spending from yesterday is already categorized automatically.

Commute: Your payment fintech app notifies you that your weekly transport card reload has been processed. No manual top-up needed.

Lunch: You split a meal using a peer-to-peer payment app. The request settles instantly. No IOUs, no bank transfers.

Afternoon: Your robo-advisor (WealthTech) sends a notification that your monthly contribution has been invested automatically at market open.

Evening: You check your lending fintech dashboard and see your loan repayment processed. Your credit score has been updated.

End of the month: Your InsurTech provider sends your usage-based insurance statement. You drove less this month, so your premium is lower.

Common Mistakes When Navigating Fintech Categories

1. Confusing fintech categories and assuming all fintech is the same

Many beginners treat fintech as a single category. They assume that because one fintech platform is trustworthy, all fintech platforms carry the same level of safety and regulation. In reality, a licensed neobank holding your deposits operates under completely different rules than an unregulated crypto platform. Always identify the category before assessing the risk.

2. Not understanding the risks specific to each category

Each fintech type carries its own risk profile. Crypto platforms carry market volatility risk and, in some cases, no deposit protection. BNPL lending platforms can lead to debt accumulation if misused. Even legitimate WealthTech platforms carry investment risk that regulated neobanks do not. Understanding the category helps you understand the risk.

3. Using unregulated platforms in high-risk categories

Blockchain fintech and newer lending platforms are the categories where unregulated players are most common. Before using any platform in these categories, verify that it holds the appropriate regulatory authorization in your country. Regulation is not a guarantee of performance, but its absence is a serious warning sign.

4. Overusing multiple overlapping apps

With fintech available across seven categories, it is easy to accumulate five payment apps, three budgeting tools, and two investment accounts that all perform similar functions. This creates confusion, increases security exposure, and typically means you use none of them well. Build deliberately across categories, not randomly within them.

5. Ignoring security practices across multiple platforms

More fintech accounts mean more attack surface for fraud and unauthorized access. Use unique, strong passwords for every platform. Enable two-factor authentication on all financial apps. Review account activity regularly. The convenience of fintech is worth protecting with basic security discipline.

Conclusion

Fintech is not one thing. It is a collection of specialized industries, each using technology to solve a different financial problem. Understanding the categories helps you use these platforms more confidently, assess them more critically, and build a personal finance approach that draws on the best of each segment.

Here is what to carry forward from this guide:

The seven main fintech types are payments, lending, WealthTech, InsurTech, RegTech, blockchain fintech, and neobanks

Each category exists because it solves a specific financial problem that traditional institutions handled poorly

Different categories carry different regulations, risk profiles, and revenue models

The most effective personal finance approach combines specialist platforms across categories rather than relying on one all-in-one solution

Always identify which fintech category a platform belongs to before connecting your financial accounts or trusting it with your money

Security, regulation, and category understanding are the three filters that protect you in a world of hundreds of financial apps

Frequently Asked Questions

Q: What are the main types of fintech?

The seven main types of fintech are payment fintech, lending fintech, WealthTech, InsurTech, RegTech, blockchain fintech, and neobanks or digital banks. Each category addresses a different area of financial services using technology to deliver faster, cheaper, and more accessible products than traditional institutions offer.

Q: How many types of fintech exist?

Industry analysts commonly identify seven major fintech categories, though some frameworks add additional subcategories such as PropTech for property finance and HealthTech for health-related financial products. The seven core categories covered in this guide represent the vast majority of fintech companies, users, and investments globally. The boundaries between categories are not rigid, and many companies operate across multiple segments.

Q: What is the biggest fintech category?

Payment fintech is the largest category by transaction volume, user numbers, and total revenue. Digital payments represent hundreds of trillions of dollars in annual value processed globally, and the companies that move that money are among the highest-valued in the entire financial technology industry. Lending fintech is the second largest by total loan book value, followed by WealthTech by assets under management.

Q: What is the difference between neobanks and traditional banks?

Traditional banks operate through physical branch networks, legacy technology systems, and processes built over decades. They typically carry higher fees, slower account opening, and more complex customer service requirements. Neobanks operate entirely digitally with no physical branches, modern cloud-based infrastructure, and interfaces optimized for mobile use. Most neobanks offer zero-fee accounts, instant setup, and real-time transaction data. The key practical difference for users is speed, cost, and user experience. For regulatory purposes, neobanks in most jurisdictions hold banking licenses or partner with licensed institutions to provide deposit protection equivalent to traditional banks.

Q: Which fintech type is most popular with everyday users?

Payment fintech is the most widely used category by everyday users because digital payments touch every purchase. The second most popular category for everyday users is neobanks, driven by the adoption of mobile-first banking apps that offer better interfaces and lower fees than traditional current accounts. WealthTech is the fastest-growing category among users under 35, driven by the widespread adoption of commission-free investment apps that made investing accessible to people who previously had no entry point into financial markets.

Share this article

Related Articles

10 Best Fintech Companies in the UK You Must Know

Discover the 10 best fintech companies in the UK for banking, payments, lending, and business finance. Compare Revolut, Wise, Monzo, Starling, and more to choose the right fintech solution.

Top 20 Fintech Companies in the USA Leading Financial Innovation

Discover the 20 best fintech companies in the USA transforming banking, payments, investing, and lending. Compare top innovators to find the right financial technology solution.

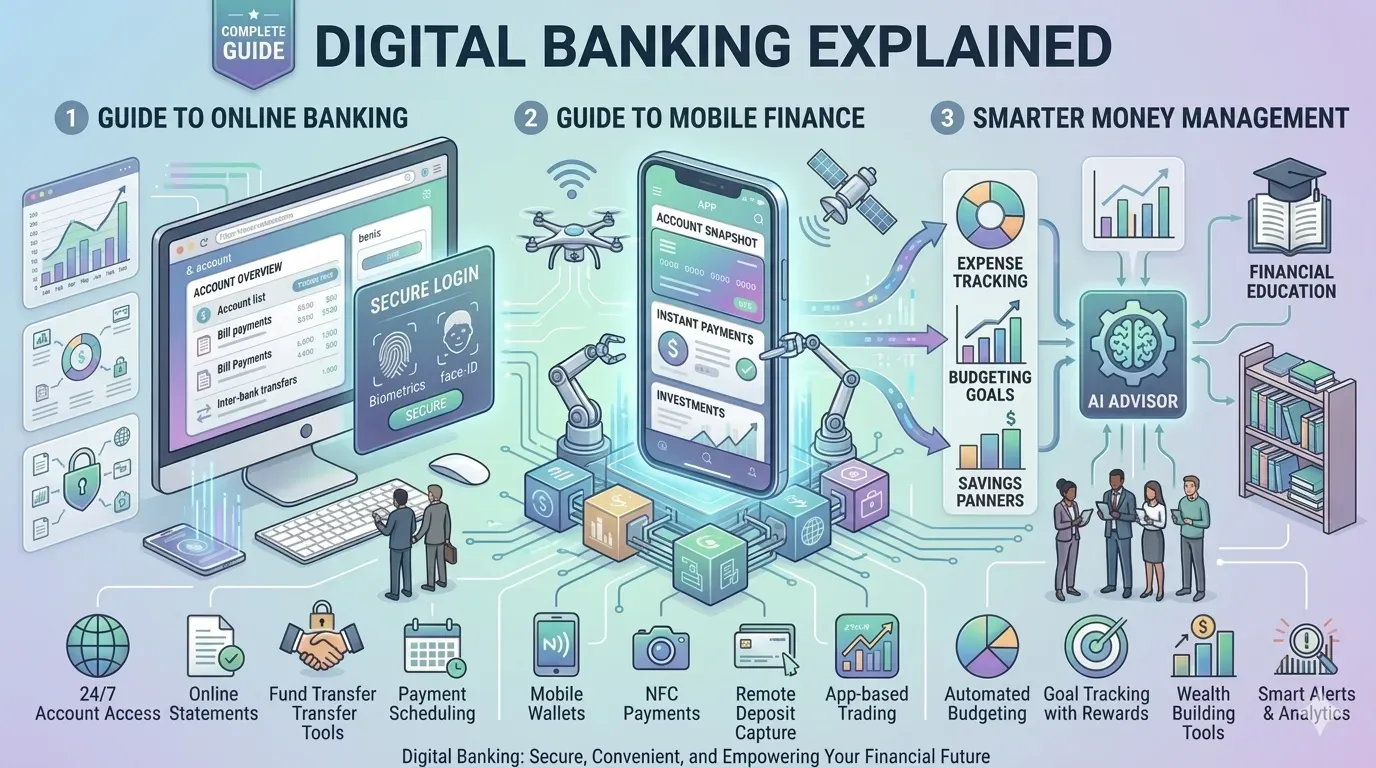

Digital Banking Explained: A Complete Guide to Online Banking, Mobile Finance, and Smarter Money Management

Discover digital banking in 2026 with online banking, mobile finance apps, secure payments, and smart tools that make managing money easier, faster, and safer.