Digital Banking Explained: A Complete Guide to Online Banking, Mobile Finance, and Smarter Money Management

Discover digital banking in 2026 with online banking, mobile finance apps, secure payments, and smart tools that make managing money easier, faster, and safer.

The Way We Bank Has Fundamentally Changed

Not long ago, managing your money meant visiting a bank branch, filling out forms, standing in queues, and waiting days for basic transactions to clear. That experience frustrated millions of people, but there was no real alternative. Banking was simply inconvenient, and customers accepted it.

Then digital banking arrived and changed everything.

Today, you can open a bank account in minutes from your sofa. You can transfer money to the other side of the world in seconds. You can see every transaction the moment it happens, set savings goals, track your spending by category, pay bills automatically, and get a complete picture of your financial health without ever speaking to a single bank employee.

Digital banking is not just a more convenient version of traditional banking. It is a fundamentally different relationship between people and their money. It gives individuals more visibility, more control, and more tools than any previous generation of bank customers has ever had.

This guide covers everything you need to know about digital banking. You will learn what it is, how it works, what features it offers, how to use it effectively, and how to avoid the most common mistakes people make when managing money online.

What Is Digital Banking?

A Simple, Clear Definition

Digital banking is the delivery of banking products and services through digital channels, primarily mobile apps and websites, rather than through physical branches. It covers everything from checking your balance and making payments to applying for loans, setting up savings goals, and managing your entire financial life from a single screen.

Digital banking is not a single product. It is a category that includes the online banking portals of traditional banks, the apps of dedicated digital banks, and the platforms of fintech companies that offer banking-adjacent services. What unites them all is the delivery method: technology replaces the branch as the primary point of contact between the customer and the bank.

"Digital banking is not just banking on a screen. It is a complete reimagining of how financial services are designed, delivered, and experienced by everyday people."

Digital Banking vs Traditional Banking vs Neo Banking

These three terms are related but distinct, and many people confuse them.

Traditional banking uses physical branches as its primary service channel, supplemented by digital tools. Your local bank with a high street branch is a traditional bank, even if it also has a mobile app.

Digital banking refers to banking delivered primarily through digital channels. Traditional banks that have invested heavily in their online and mobile platforms offer digital banking services, even though they still have branches.

Neo banking refers to entirely digital banks with no physical branches. Neo banks are the purest form of digital banking. They exist only as apps and websites, and they are built from the ground up on modern technology.

In practice, when people say digital banking, they often mean any banking done online or through an app. This guide uses that broader definition while drawing distinctions where they matter.

Why Digital Banking Has Grown So Fast

The growth of digital banking has been driven by several forces working together. Smartphone adoption has made powerful computing devices available to almost everyone. Faster internet connections have made real-time data transfers routine. Customer expectations have risen as people experienced the speed and convenience of other digital services and began demanding the same from their banks.

The global pandemic accelerated this shift dramatically. Millions of people who had avoided digital banking out of habit or unfamiliarity were suddenly unable to visit branches. Many discovered that digital banking was not just adequate but actually better for most of their everyday needs. A large proportion of those people never went back to branch-based banking for routine tasks.

How Digital Banking Works?

The Technology Behind the Experience

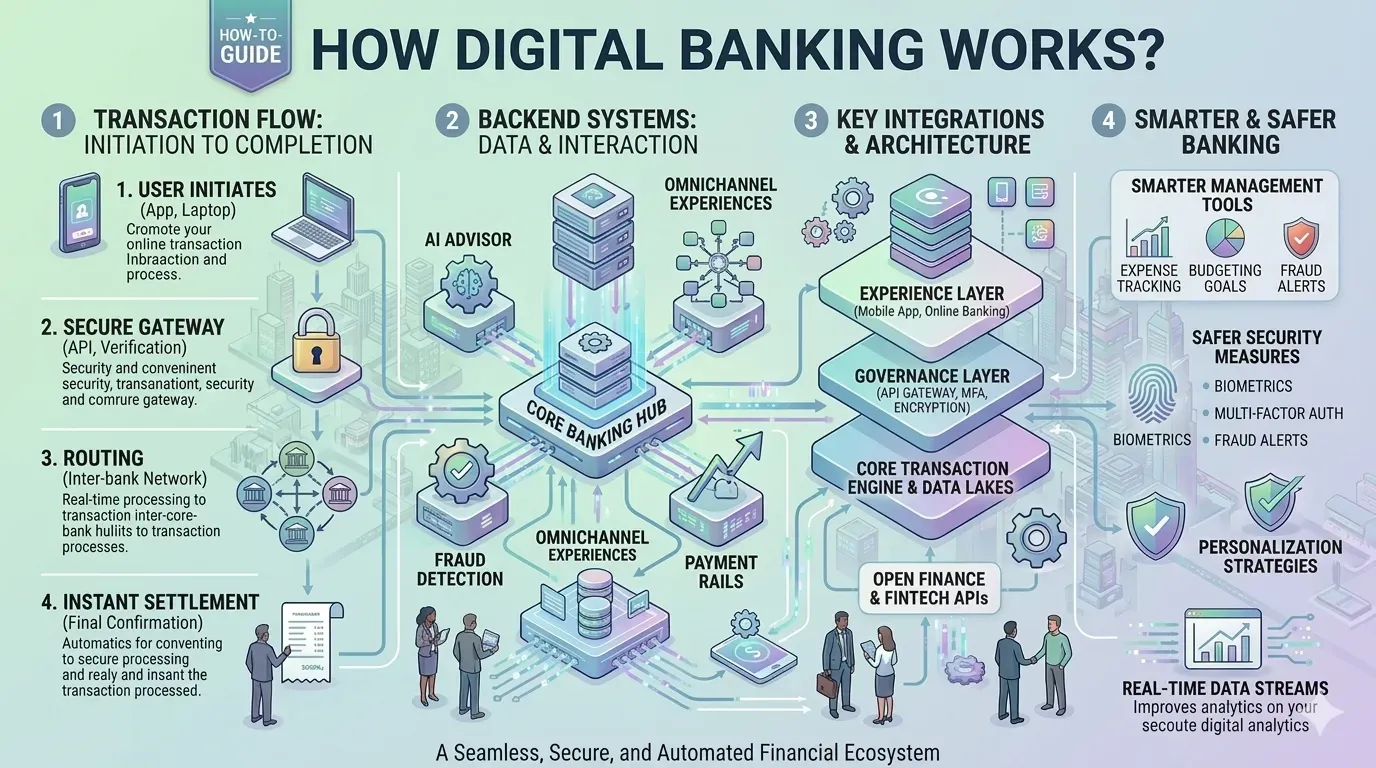

Digital banking relies on a combination of technologies working together to deliver a seamless experience. At the core is the bank's core banking system, which processes transactions and maintains account records. On top of this sits a digital layer: the app or website that customers interact with, connected to the core system through secure APIs.

APIs, or Application Programming Interfaces, are what make modern digital banking possible. They allow the customer-facing app to communicate with the bank's systems in real time, pulling your balance, processing a payment, or updating a savings goal the moment you tap a button. APIs also allow digital banks to connect with third-party services, payment networks, identity verification systems, and financial data providers.

How Online Transactions Work?

When you make a payment through a digital banking app, a sequence of events happens almost instantly. Your app sends an encrypted request to the bank's servers. The server checks your balance and the legitimacy of the transaction. If everything checks out, it sends an instruction to the relevant payment network, which moves the money to the recipient's bank. The whole process, which once took days through paper-based clearing systems, now takes seconds.

Security Architecture in Digital Banking

Digital banking security operates on multiple layers. The first layer is authentication. You prove who you are using a passcode, fingerprint, or face recognition. The second layer is encryption. All data travelling between your app and the bank's servers is encrypted, so it cannot be read if intercepted. The third layer is fraud detection. Banks use machine learning systems to monitor transaction patterns and flag anything unusual for review.

In real life, the biggest security risks in digital banking come not from failures in this technical architecture but from human error. Phishing scams, weak passwords, and sharing login details are responsible for the vast majority of digital banking fraud. The system is built to be secure. The challenge is using it securely.

Digital Onboarding

One of the most significant innovations digital banking brought to the industry is the ability to open an account entirely online. Here is how a typical digital onboarding process works.

You visit the bank's website or download its app.

You enter your personal details, including your name, date of birth, and address.

You verify your identity by uploading a photo of your passport or national ID.

You take a selfie, which the system compares to your ID photo.

The bank's automated verification system checks your details, usually within minutes.

Your account is approved, and you will receive access immediately.

A physical debit card is mailed to you, while a virtual card is available in the app right away.

Many beginners are surprised by how fast this process is. What once took a branch visit, a waiting period, and a follow-up appointment now happens on a phone screen before your morning coffee gets cold.

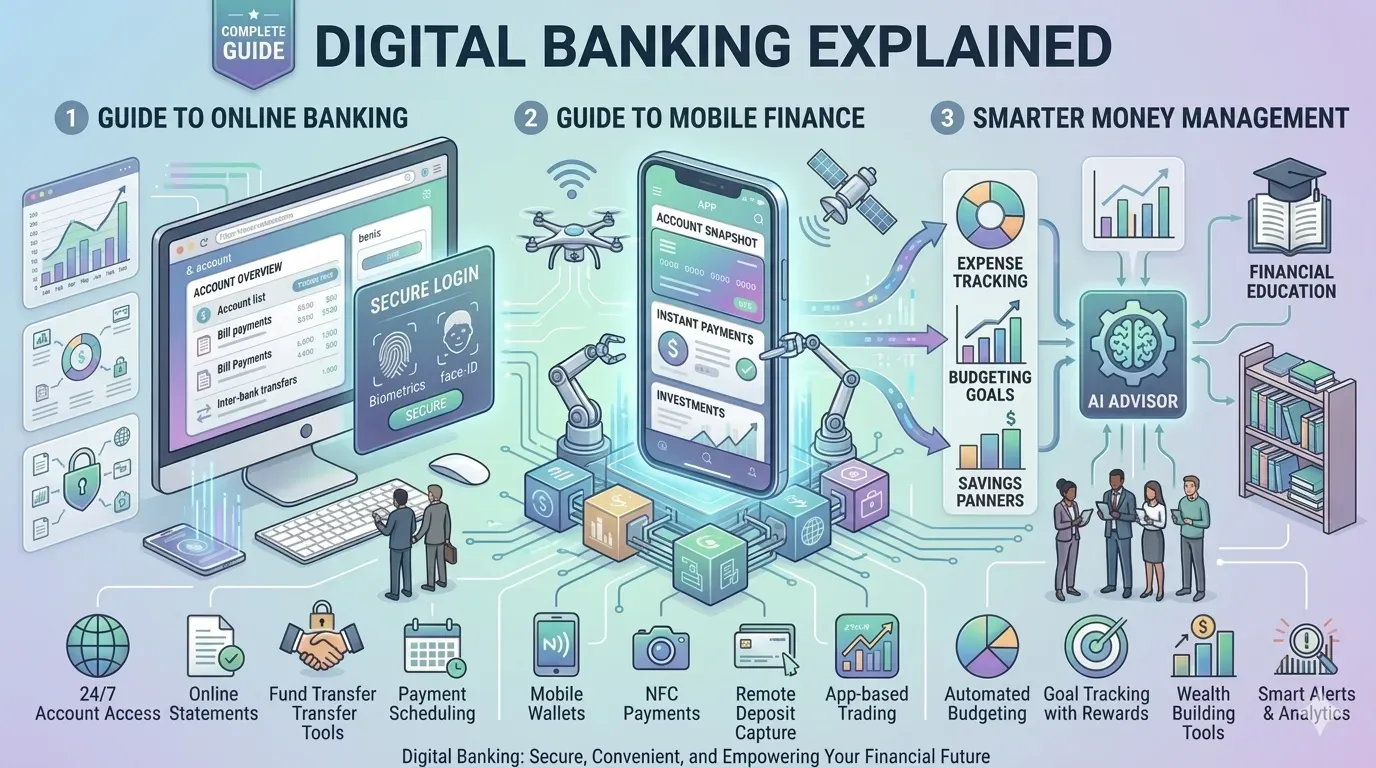

Key Features of Digital Banking

Real-Time Account Access

The most fundamental feature of digital banking is access to your account information at any time, from anywhere. Your balance, recent transactions, upcoming payments, and account statements are all available instantly through your app or online portal. There is no need to visit a branch or wait for a monthly paper statement.

Instant Payments and Transfers

Digital banking has transformed the speed of money movement. Payments between accounts at the same bank are typically instant. Transfers to accounts at other banks, which once took 1 to 3 business days through traditional clearing systems, now complete in seconds via modern payment infrastructure in many countries.

International transfers, which can still take time and incur significant fees at traditional banks, are increasingly being handled by digital banking platforms and specialist fintech services at lower costs and faster speeds.

Expense Tracking and Spending Categories

Digital banking apps automatically categorize every transaction you make. Groceries, dining, transport, entertainment, subscriptions, and shopping are all sorted without any effort from you. At a glance, you can see exactly how much you spent in each category over any given period.

From a practical perspective, this automatic categorization removes the single biggest barrier to understanding your spending: the effort of tracking it manually. Most people who start using expense tracking through their digital bank report being genuinely surprised by where their money actually goes, as opposed to where they thought it went.

Budgeting Tools

Building on expense tracking, most digital banking platforms let you set monthly spending limits for each category. You decide how much you want to spend on dining out, entertainment, or personal shopping each month. The app tracks your progress against those limits and sends you alerts when you are approaching them.

This turns budgeting from a discipline that requires willpower into a system that runs automatically in the background. You set the rules once. The app enforces them every day.

Savings Goals and Pots

Digital banking platforms typically offer savings pots or vaults, which are ring-fenced areas within your account for specific goals. You create a pot for your emergency fund, your next holiday, a new car, or a house deposit. You give it a target amount and a target date. The app tracks your progress and can automatically move money into the pot on a schedule you set.

Round-up features take this further. Every time you make a purchase, the app rounds up to the nearest whole number and moves the difference into your savings pot. Spending 4.30 on lunch automatically sends 70 pence toward your holiday fund. These small amounts accumulate faster than most people expect.

Financial Dashboard

A good digital banking app gives you a complete financial dashboard that shows your income, your spending by category, your savings progress, your upcoming bills, and your overall cash flow in one view. This level of financial visibility was previously available only to people who maintained detailed spreadsheets or paid for financial planning software. Digital banking delivers it automatically to every account holder.

Virtual and Physical Cards

Digital banking accounts come with both virtual cards, available in the app immediately, and physical debit cards sent by post. Virtual cards can be added to mobile payment wallets like Apple Pay or Google Pay and used for online purchases. Many digital banking platforms also offer disposable virtual card numbers for secure online shopping, reducing the risk of your card details being compromised.

In-App Customer Support

Customer support in digital banking happens through the app itself, via chat, email, or in some cases, phone. Many digital banks use AI-powered chatbots for common queries, with human agents available for complex issues. Response times through in-app chat are often faster than waiting in a branch queue or on hold with a traditional bank's phone line.

The Real Benefits of Digital Banking

Lower Costs and Fewer Fees

Digital banks carry significantly lower operating costs than traditional banks. Without a branch network to maintain, thousands of branch staff to pay, and physical infrastructure to manage, digital banks can pass those savings directly to customers through lower fees, better exchange rates, and higher interest on savings.

Many digital banking accounts charge no monthly fees, no overdraft fees for small amounts, and no foreign transaction fees. For customers who travel regularly or make international purchases, these savings can be substantial.

Speed and Convenience

Speed is perhaps the most immediately obvious benefit of digital banking. Payments happen in seconds. Account opening takes minutes. Statements are available instantly. Problems can be reported and often resolved through the app without speaking to anyone. The time cost of banking, which used to be measured in hours of branch visits and phone calls, shrinks to minutes.

"In real life, the average person spends over 10 hours a year on banking administration. Digital banking cuts that to under 2 hours for most customers. That time is genuinely given back to you."

Complete Financial Visibility

Digital banking gives you a level of insight into your own financial behavior that was simply not available before. When every transaction is automatically tracked, categorized, and visualized, patterns become visible. You can see which subscriptions are draining your account, which spending categories consistently exceed your budget, and how your saving habits are evolving. This visibility is the foundation of genuine financial improvement.

Smarter Money Management

The combination of expense tracking, budgeting tools, savings goals, and financial dashboards turns a digital banking app into a personal finance system. You do not need separate budgeting software or financial planning apps. Everything you need to understand and manage your money is built into your bank account.

Accessibility and Inclusion

Digital banking removes many of the barriers that prevent people from accessing financial services. No branch within traveling distance. No time to visit during business hours. Physical mobility challenges. Language barriers in branch environments. Digital banking addresses all of these. A smartphone and an internet connection are all you need to access a full-featured bank account.

Continuous Improvement

Traditional banks update their products slowly. Digital banks update their apps continuously. New features, improved interfaces, better tools, and enhanced security arrive through regular app updates. The product you use today is better than the one you signed up for six months ago, and it will be better again in six months.

How to Use Digital Banking Effectively?

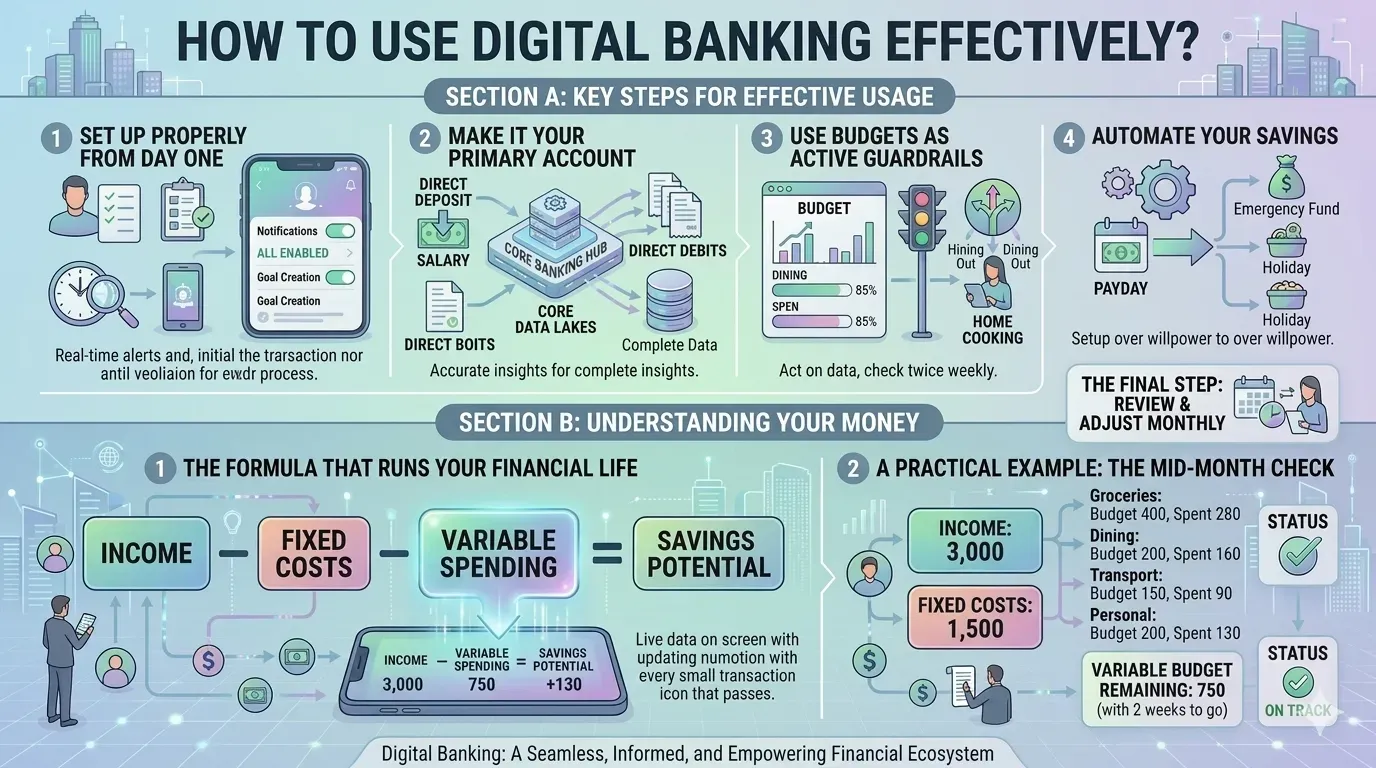

Set It Up Properly From Day One

The quality of your digital banking experience depends heavily on how well you set it up at the start. Enable all notifications, so you receive real-time alerts for every transaction. Set up your spending categories and review that the automatic categorization matches how you actually think about your spending. Create savings pots for your key financial goals before you start spending from the account.

Make It Your Primary Account

Digital banking works best when all your income flows through it. Have your salary deposited directly. Set up all your regular bills and direct debits. The more of your financial life runs through the account, the more complete and accurate the data the app has to work with, and the more useful its insights become.

Use Budgets as Active Guardrails

Setting a budget is only the first step. The real value comes from checking it regularly and letting it influence your decisions. When your app tells you that you have used 85 percent of your dining budget with ten days left in the month, that information is only useful if you act on it. Check your budget progress at least twice a week. Let the numbers guide your choices.

Automate Your Savings

Set up automatic transfers to your savings pots on payday. Move money into your savings goals before you have a chance to spend it. Even small automatic transfers, 50 or 100 per month to each goal, build significant balances over time. The key is automation. Manual transfers rely on willpower. Automatic transfers rely on setup.

Review and Adjust Monthly

At the end of each month, spend twenty minutes reviewing your complete financial picture. Look at your total spending by category, compare it to your budgets, assess your savings progress, and decide what adjustments to make for the coming month. This monthly review is where real financial improvement happens.

Understanding Your Money Through Digital Banking

The Formula That Runs Your Financial Life

Income − Fixed Costs − Variable Spending = Savings Potential

Every personal finance decision you make connects back to this formula. Your income is fixed in the short term. Your fixed costs, rent, utilities, and loan repayments, are largely fixed too. The variable spending in the middle is where all your financial decisions happen. And the result of those decisions determines how much you can save.

A digital banking app makes this formula visible in real time. You can see your income the moment it arrives, watch your fixed costs leave automatically, track your variable spending as it happens, and see your remaining balance update with every transaction. The formula is no longer theoretical. It is live data on your phone screen.

A Practical Example

Imagine you earn 3,000 per month. Your fixed costs total 1,500. Your digital banking app tracks your variable spending across the month, and you can see in real time how that remaining 1,500 is being used.

You have set budgets of 400 for groceries, 200 for dining out, 150 for transport, and 200 for personal spending. You have automatic transfers of 300 to your emergency fund and 250 to your holiday savings pot set up for payday.

By the middle of the month, your app shows that you have spent 280 on groceries, 160 on dining, 90 on transport, and 130 on personal spending. You have 750 of your variable budget remaining with two weeks to go. You are on track. You know this not because you sat down with a spreadsheet but because your digital banking app showed you in thirty seconds when you opened it this morning.

This is what effective digital banking looks like in daily life. Not complicated. Not time-consuming. Just consistently informed.

Combining Digital Banking With Smart Financial Habits

The Power of the Combined Approach

Digital banking provides the tools. Good financial habits determine how much value you extract from them. The most financially successful digital banking users are not those with the most sophisticated apps. They are the ones who engage with their app consistently and use what it shows them to make better decisions.

Daily Routine (3 to 5 Minutes)

Open your app and check your current balance.

Review any new transactions from the past 24 hours.

Check for any alerts or unusual activity.

Note where you are against your most active spending categories.

Weekly Routine (10 to 15 Minutes)

Review your spending by category for the week.

Check your budget progress for each category.

Review your savings pot balances and progress toward goals.

Identify any categories where you are running ahead of budget and adjust behavior.

Transfer any surplus funds to savings if your budget allows.

Monthly Routine (20 to 30 Minutes)

Review your complete monthly spending report.

Compare this month to the previous month and identify trends.

Assess progress toward each savings goal.

Adjust budget limits for the coming month based on what you learned.

Review all subscriptions and recurring payments and cancel any you no longer use.

Set your financial intention for the coming month.

Following this routine consistently for three months transforms most people's relationship with their money. The combination of visibility, habit, and the powerful tools digital banking provides creates genuine, lasting financial improvement.

Common Mistakes Digital Banking Users Make

Ignoring Transaction Alerts

Real-time transaction alerts are one of the most valuable features digital banking offers, and one of the most commonly disabled. Many users turn them off because they feel intrusive. This is a significant mistake. Alerts catch fraudulent transactions immediately, remind you of spending patterns in the moment, and keep you connected to your financial reality throughout the day. Keep them on.

Not Exploring the Full Feature Set

Most digital banking users use about 20 percent of their app's features. They check their balance, make payments, and ignore everything else. Savings pots, budgeting tools, spending analytics, round-up features, and financial dashboards remain untouched. These features exist to make your financial life better. Take two hours to explore your app fully. You will find tools you did not know existed and wish you had been using all along.

Using Multiple Apps Instead of One System

Some people have a digital banking account for everyday spending, a separate budgeting app, a different savings app, and a spreadsheet for tracking. The result is fragmented data, duplicated effort, and a financial picture that nobody, including themselves, fully understands. Modern digital banking apps are designed to replace all of these. Let them.

Neglecting Security Best Practices

Digital banking security is only as strong as your personal security habits. Use a strong, unique passcode. Enable biometric login. Never share your login details with anyone. Do not access your banking app on public Wi-Fi without a VPN. Be skeptical of any message, email, or phone call asking you to confirm your banking details. Banks never ask for your full password or PIN through these channels.

Spending Without Reviewing

The most common failure in digital banking is the simplest. People open accounts, enjoy the convenience, and then stop engaging with the financial management features entirely. They spend money, get paid, spend more money, and never look at the spending summaries or budget progress. The tools are there. They are not working. All the technology in the world cannot help someone who is not paying attention.

Not Keeping an Emergency Fund

Many digital banking users use their accounts for spending and save nothing. A single unexpected expense, a car repair, a medical bill, or a broken appliance, wipes out their balance and sends them into overdraft or debt. Every digital banking account should have a dedicated emergency fund pot with at least one month of living expenses. Work toward three to six months over time. This single habit protects your financial life more than any other.

Conclusion

The shift to digital banking is not coming. It has already happened. Millions of people around the world now manage their entire financial lives through apps and websites. They pay less in fees, move money faster, save more consistently, and understand their spending more clearly than any generation before them. They do this not because they are particularly disciplined or financially sophisticated. They do it because digital banking makes good financial habits easy.

Traditional banking still has a role. Complex financial products, in-person advice for major life decisions, cash handling, and the security of long-established regulatory frameworks all remain valuable. The smartest approach combines the strengths of both systems, using digital banking for the speed, visibility, and money management tools it excels at, while relying on traditional banking where its depth of products and physical presence genuinely add value.

But the center of gravity has shifted. The branch is no longer the heart of banking. The app is. And the app is getting better, faster, and more powerful with every passing month.

If you are not yet using digital banking to its full potential, the cost is real. You are paying fees you do not have to pay, missing insights you could be acting on, and leaving tools unused that could genuinely change your financial life. The barrier to entry is low. The upside is significant. Start today, stay consistent, and let the technology do what it was built to do.

Frequently Asked Questions

Q: What is digital banking?

Digital banking is the delivery of banking services through online and mobile channels rather than physical branches. It includes everything from checking your balance and making payments to applying for loans, setting savings goals, and managing your complete financial life through an app or website. It covers both the digital services of traditional banks and the fully online platforms of digital-only banks.

Q: How does digital banking work?

Digital banking works through a combination of secure apps or websites, connected to the bank's core systems through encrypted APIs. When you make a transaction, the app communicates with the bank's servers in real time, processing the payment and updating your account balance instantly. All data transfers are encrypted. Your identity is protected by authentication methods including passcodes, fingerprints, and facial recognition.

Q: Is digital banking safe?

Yes, digital banking is safe when used correctly. Reputable digital banks operate under the same regulatory frameworks as traditional banks, with encryption, fraud detection systems, and deposit protection schemes protecting customer funds and data. The main security risks come from user behavior rather than system failures. Using strong passwords, enabling biometric authentication, and staying alert to phishing attempts keep your digital bank account secure.

Q: What are the best features of digital banking?

The most valuable features of digital banking include real-time transaction notifications, automatic expense categorization, budgeting tools with spending limits, savings pots for specific goals, round-up saving features, financial dashboards that visualize your complete money picture, instant payments, and in-app customer support. These features, used consistently, give you more control over your money than any previous generation of bank customers has ever had.

Q: How do beginners get started with digital banking?

Start by choosing a digital bank available in your country and downloading its app. Complete the digital onboarding process, which typically takes five to ten minutes and requires only your ID and a selfie. Add money to your account by bank transfer. Then spend time exploring the app's features: set up your spending budgets, create savings pots for your goals, enable all notifications, and schedule an automatic savings transfer for your next payday. You will be set up for effective digital money management within an hour.

Q: What is the difference between digital banking and mobile banking?

Mobile banking specifically refers to banking done through a smartphone app. Digital banking is a broader term that includes mobile banking as well as online banking done through a web browser on a computer or tablet. In practice, most digital banking today is predominantly mobile banking, since the majority of users access their accounts through their phones rather than desktop browsers.

Share this article

Related Articles

10 Best Fintech Companies in the UK You Must Know

Discover the 10 best fintech companies in the UK for banking, payments, lending, and business finance. Compare Revolut, Wise, Monzo, Starling, and more to choose the right fintech solution.

Top 20 Fintech Companies in the USA Leading Financial Innovation

Discover the 20 best fintech companies in the USA transforming banking, payments, investing, and lending. Compare top innovators to find the right financial technology solution.

Traditional Banking Explained: A Complete Guide to How Banks Work, What They Offer, and How to Use Them Effectively

Understand traditional banking in simple terms. This guide explains how banks work, the services they offer, and how to use them effectively for saving, loans, and everyday financial needs.