Traditional Banking Explained: A Complete Guide to How Banks Work, What They Offer, and How to Use Them Effectively

Understand traditional banking in simple terms. This guide explains how banks work, the services they offer, and how to use them effectively for saving, loans, and everyday financial needs.

Most people open their first bank account before they fully understand what a bank actually does. They deposit money, use a debit card, pay bills, and move on. Banking stays in the background, quiet and mostly invisible, until something goes wrong.

But traditional banking is far more than a place to store your salary. It is one of the oldest and most powerful financial systems in human history. It shapes how businesses grow, how families buy homes, how governments manage economies, and how individuals build financial security over a lifetime.

At the same time, traditional banking has real limitations. Hidden fees, slow processes, rigid requirements, and outdated technology frustrate millions of customers every year. Understanding how the system works gives you the power to use it on your own terms, avoid its pitfalls, and make smarter decisions about your money.

This guide covers everything you need to know about traditional banking. You will learn what it is, how it works, what it offers, and how to use it effectively alongside modern financial tools.

What Is Traditional Banking?

A Simple, Clear Definition

Traditional banking refers to the financial services provided by licensed banks through a combination of physical branches and digital channels. These banks accept deposits from customers, lend money to borrowers, process payments, and offer a range of financial products, including savings accounts, loans, mortgages, and investment services.

Traditional banks have a physical presence. They operate branch networks where customers can walk in, speak with a banker, deposit cash, get advice, and handle complex financial transactions face to face. They also offer online and mobile banking as supporting tools, though the physical branch remains central to their identity.

"Traditional banking is the foundation of the modern financial system. Every salary you receive, every mortgage you take, and every payment you make passes through this network in some form."

A Brief History of Traditional Banking

Banking as a formal system began in medieval Europe, where merchants needed safe places to store gold and a reliable way to transfer wealth across distances. Early banks issued paper receipts for deposits, which eventually evolved into the banknotes and electronic records we use today.

Over centuries, banks grew into regulated institutions backed by governments and central banks. Today, traditional banking operates under strict regulatory frameworks designed to protect depositors, maintain financial stability, and prevent fraud.

Traditional Banking vs Digital Banking

Traditional banks have physical branches. Digital banks operate entirely online.

Traditional banks offer face-to-face customer service. Digital banks use chat and email support.

Traditional banks often charge higher fees. Digital banks typically charge less.

Traditional banks process some transactions more slowly. Digital banks move money faster.

Traditional banks offer a wider range of complex financial products. Digital banks focus on core everyday banking.

Traditional banks are better for cash handling, complex loans, and in-person advice. Digital banks are better for speed, convenience, and modern money management tools.

Neither system is universally better. The right choice depends on what you need from your bank. Many smart consumers use both systems in combination.

How Traditional Banking Works?

The Core Banking Model

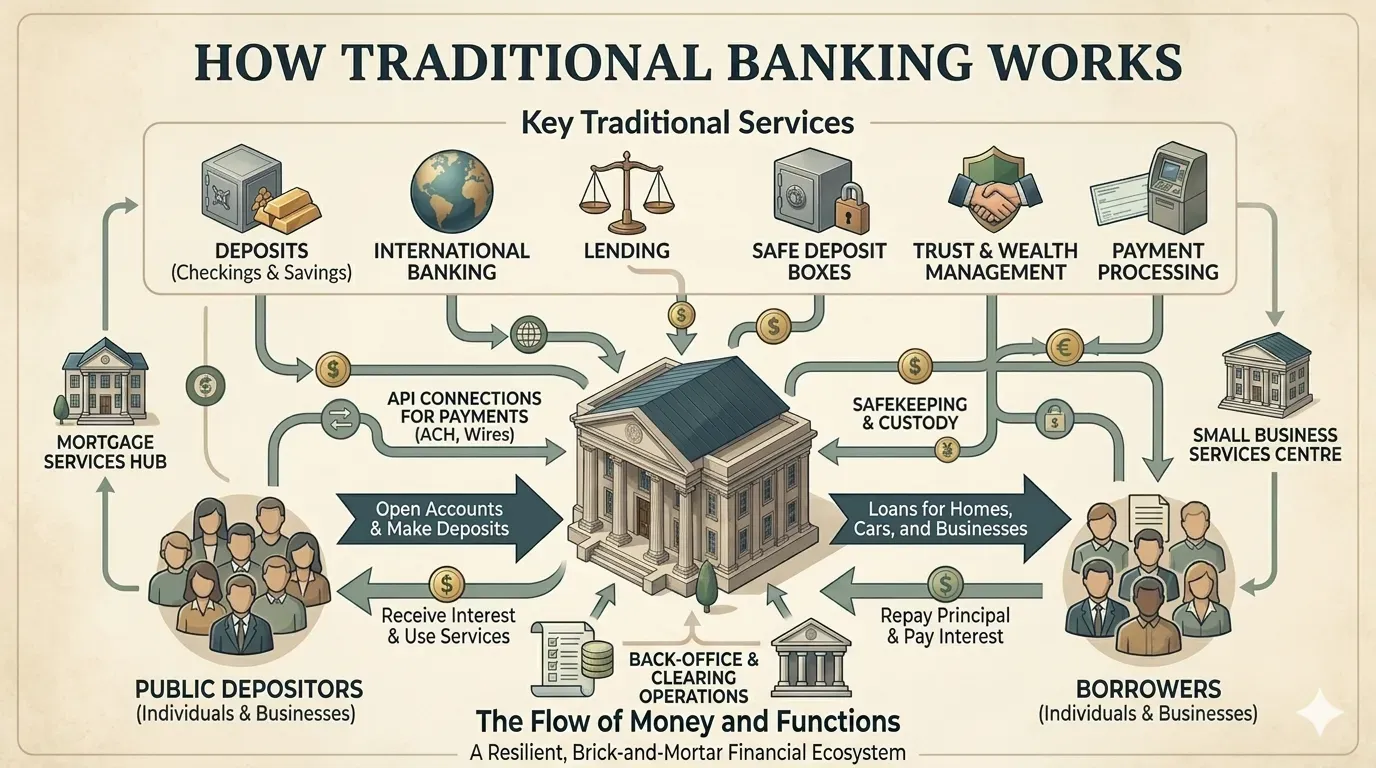

Traditional banks operate on a model that has remained fundamentally consistent for centuries. They collect deposits from customers who want a safe place to store money. They pay those customers interest on their deposits. Then they lend that deposited money to other customers, businesses, and governments at a higher interest rate. The difference between the interest they pay on deposits and the interest they earn on loans is called the net interest margin. That margin is how banks make money.

This system means that your savings account is not just a storage box. When you deposit money in a bank, that bank uses it to fund loans for other people. The bank guarantees that your money is available when you need it, but it is constantly working behind the scenes to generate returns.

The Role of Central Banks

Traditional banks do not operate in isolation. Every country has a central bank, such as the Federal Reserve in the United States, the Bank of England in the UK, or the State Bank of Pakistan, that regulates commercial banks, sets interest rates, and manages the money supply.

Central banks act as a lender of last resort. If a commercial bank faces a liquidity crisis, the central bank can step in to provide emergency funding. This backstop is part of what makes deposits in regulated traditional banks relatively safe.

How Deposits and Loans Work Together?

Here is a simplified version of how the system flows. A customer deposits 10,000 in a savings account. The bank pays that customer 2 per cent annual interest, which is 200 per year. The bank then lends that 10,000 to a borrower at 7 per cent annual interest, earning 700 per year. The 500 difference covers the bank's operating costs and generates profit.

This process, repeated millions of times across millions of accounts, is the engine of the traditional banking system.

Fractional Reserve Banking

Traditional banks do not keep all your deposited money sitting in a vault. They are required by regulation to keep only a fraction of deposits in reserve, typically a small percentage. The rest they lend out. This is called fractional reserve banking, and it is how a relatively small amount of actual currency in circulation supports a much larger economy.

In real life, this means that if a large number of depositors tried to withdraw all their money at the same time, a bank could face serious problems. This is called a bank run, and it is why regulatory frameworks, deposit insurance schemes, and central bank oversight exist.

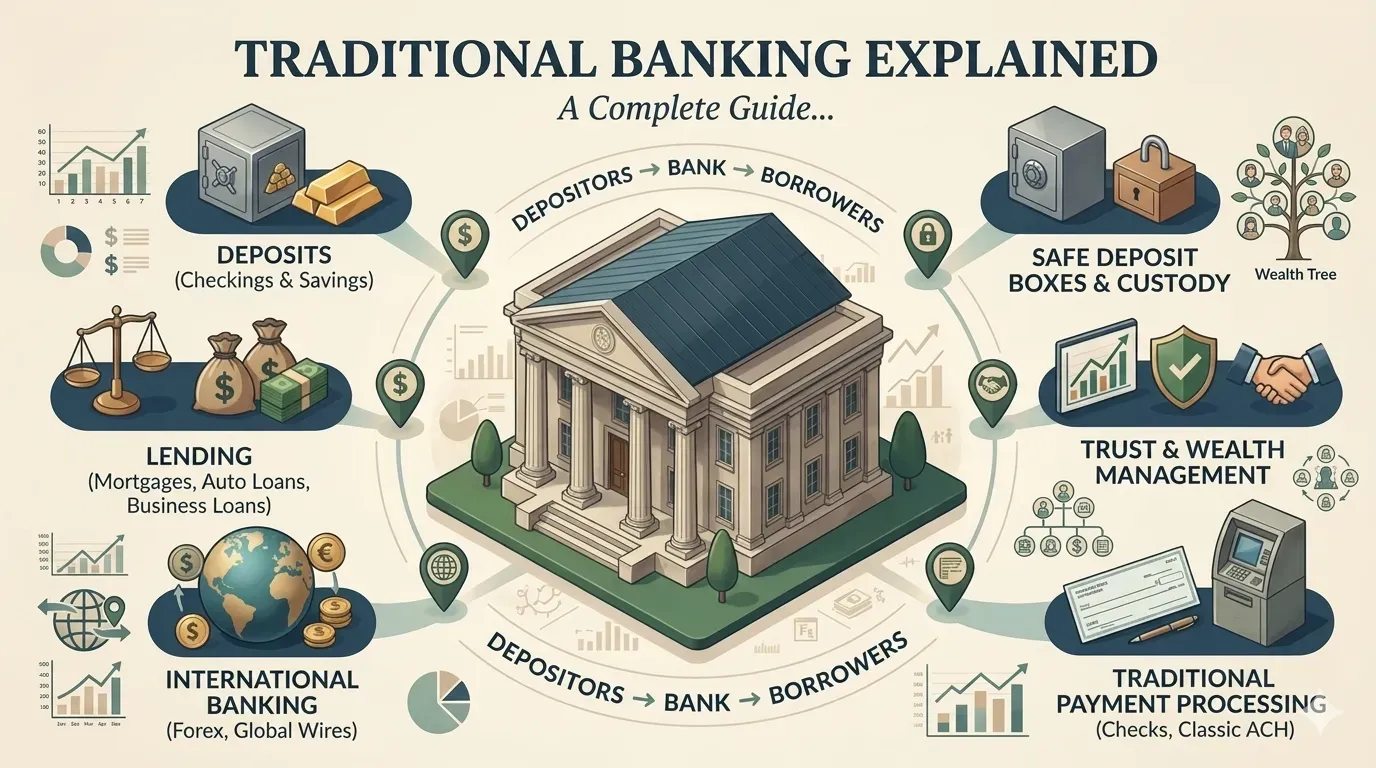

Key Features of Traditional Banking

Branch Network and In-Person Service

The defining feature of traditional banking is physical access. Branches give customers a place to deposit cash, get certified documents, discuss complex financial products, resolve disputes, and receive personalised advice from trained staff.

For many customers, especially older generations and those dealing with complex financial situations, the ability to walk into a branch and speak to a human being is not just convenient. It is essential.

Current and Savings Accounts

Traditional banks offer current accounts for everyday spending and savings accounts for storing money over time. Current accounts come with a debit card, a chequebook in some markets, and access to online banking. Savings accounts offer interest on deposited funds in exchange for less immediate access.

Many traditional banks also offer fixed-term deposits, which lock your money away for a set period at a higher interest rate. This suits customers who want to grow their savings without the temptation of easy access.

Loans and Mortgages

Traditional banks are the primary source of lending for most consumers and businesses. They offer personal loans for large purchases, mortgages for property, car finance, business loans, and credit cards.

The lending process involves a credit assessment. The bank reviews your income, credit history, existing debts, and overall financial health before approving a loan. This process can feel slow and intrusive, but it exists to protect both the borrower and the bank.

Debit and Credit Cards

Traditional banks issue debit cards linked directly to your current account and credit cards that extend a line of credit. Credit cards in particular come with consumer protections, rewards programs, and fraud liability limits that make them a powerful tool when used responsibly.

Online and Mobile Banking

Most traditional banks now offer digital banking services alongside their branch network. You can check balances, transfer money, pay bills, and manage standing orders through an app or website. However, the digital experience at most traditional banks lags behind that of dedicated digital banks in terms of speed, design, and features.

Financial Advice and Wealth Management

Traditional banks often offer financial planning services, investment products, pension advice, and insurance. These services are particularly valuable for customers with complex financial situations, significant assets, or specific long-term goals. This is an area where traditional banks genuinely outperform digital-only alternatives.

Benefits of Traditional Banking

Trust and Security

Traditional banks have centuries of history behind them. They are licensed, regulated, and insured. In most countries, deposits up to a certain limit are protected by a government-backed deposit insurance scheme. In the United States, this is the Federal Deposit Insurance Corporation (FDIC). In the UK, it is the Financial Services Compensation Scheme (FSCS). This protection means that even if a bank fails, your money is safe up to the insured limit.

For many people, this combination of regulatory oversight, physical presence, and long institutional history creates a level of trust that newer digital banks have not yet fully earned in their minds.

Cash Handling

Traditional banks remain the primary system for handling physical cash. You can deposit coins and notes, withdraw large amounts, exchange foreign currency, and access cash through an extensive ATM network. Digital banks simply cannot match this for customers whose lives involve regular cash transactions.

Complex Financial Products

If you need a mortgage, a business loan, a structured investment product, or estate planning advice, a traditional bank with trained advisors and a full product range is hard to replace. The complexity of these products and the regulatory requirements around them means that personal guidance from an experienced banker still adds real value.

Established Relationships

One of the underrated benefits of traditional banking is the relationship you build over time with your bank. A long-standing customer with a healthy account history often receives better loan terms, higher credit limits, and more flexible treatment than a new customer at any bank, digital or traditional.

"In real life, many small business owners find that the relationship they have built with their traditional bank manager over the years is worth more than any app feature a digital bank can offer."

Wide Accessibility

For people without smartphones or reliable internet access, traditional banking remains the only practical option. Bank branches and ATMs provide financial access to populations that are digitally excluded, which is a significant portion of the global population.

How to Use a Traditional Bank Effectively?

Choose the Right Account Type

Start by understanding what you actually need. A basic current account works for everyday spending. A savings account is right for money you do not need immediate access to. A fixed-term deposit suits money you can lock away for one to five years in exchange for better interest rates. Do not pay fees for features you will never use.

Understand the Fee Structure

Many beginners make this mistake: they sign up for a bank account without reading the fee schedule. Banks charge for overdrafts, international transfers, paper statements, and sometimes even for using certain ATMs. Know what you will be charged before you commit.

Build a Strong Banking History

Your history with your bank affects your future options. Keeping your account in good standing, making regular deposits, and managing any credit products responsibly builds a positive record. This record influences your credit score, which determines the terms you receive on loans and mortgages later in life.

Use Digital Tools Alongside Branch Services

Traditional banks offer online banking for a reason. Use it. Set up automatic bill payments to avoid late fees. Download your bank's app and check your balance regularly. Set up email or SMS alerts for transactions. You get the security and full service range of a traditional bank combined with the convenience of digital access.

Negotiate When It Matters

Traditional banks have more flexibility than most customers realise. If you have a strong relationship with your bank, you can often negotiate on loan interest rates, overdraft fees, and account charges. This is especially true for business banking. Do not accept the first offer as final.

Understanding How Your Money Works Inside a Bank

The Journey of a Deposit

When you deposit money into a traditional bank account, several things happen very quickly. Your account balance is updated in the bank's core banking system. The bank records its obligation to return that money to you on demand. And behind the scenes, that deposited money becomes available for the bank to use in its lending operations.

From a practical perspective, this means your current account balance is a number on a screen representing the bank's promise to you. The actual physical currency behind that number may be anywhere in the bank's system.

The Core Formula of Traditional Banking

Deposits + Borrowed Funds = Loans + Reserves + Investments

This formula represents the basic balance sheet of a traditional bank. Everything a bank holds on one side must be matched by obligations and assets on the other. Understanding this helps you see why banks cannot simply create money from nothing and why regulatory capital requirements exist.

A Real-Life Example

Imagine a family deposits their monthly salary of 5,000 into their current account. The bank immediately records this deposit. Over the next month, the family uses 3,200 for living expenses, pays 800 in loan instalments, and leaves 1,000 sitting in the account.

The bank uses that 1,000 sitting balance, along with thousands of similar balances from other customers, to fund a mortgage for another family buying their first home. The mortgage borrower pays interest, which generates income for the bank, which allows the bank to pay interest on savings accounts, cover its operating costs, and generate profit for shareholders.

This cycle, running continuously across millions of accounts, is how traditional banking sustains itself.

Combining Traditional Banking With Modern Financial Tools

Why You Do Not Have to Choose One or the Other?

The smartest financial consumers today do not use just one banking system. They combine traditional banking with digital tools to get the best of both worlds. Your traditional bank provides security, lending capacity, cash access, and regulatory protection. Digital banking apps and neo banks provide speed, budgeting tools, real-time tracking, and lower fees for everyday transactions.

A Practical Combined Strategy

Use your traditional bank account as your primary account for salary deposits, savings, and loan products.

Use a digital banking app for everyday spending, expense tracking, and budgeting.

Transfer a set spending budget to your digital account each month and manage daily expenses through it.

Keep your savings and long-term financial products with your traditional bank, where they benefit from full regulatory protection and potentially better interest rates on larger balances.

Use your traditional bank for any transactions requiring cash, certified documentation, or in-person advice.

Daily and Weekly Routine for Combined Banking

Daily, spend two to three minutes checking your digital app for new transactions and budget alerts. Weekly, log into your traditional bank's online portal and review your savings progress, upcoming payments, and any loan statements. Monthly, conduct a full review of both accounts together to understand your complete financial picture.

From a practical perspective, this combined approach removes the frustration of traditional banking by handling routine tasks through faster, cheaper digital tools while keeping the stability, security, and full service range of a traditional bank, where it genuinely adds value.

Common Mistakes Traditional Bank Customers Make

Paying Fees Without Questioning Them

Many customers pay monthly account fees, overdraft charges, and international transfer fees for years without ever asking whether there is a better option. In real life, most banks offer multiple account tiers, and a simple conversation with your bank can often result in lower fees or a switch to a more suitable product.

Ignoring Interest Rates on Savings

Leaving large sums in a low-interest current account while better savings rates are available on the same bank's products is one of the most common and costly mistakes customers make. Always check what your bank offers across all its savings products and move money accordingly.

Not Monitoring Account Activity

Fraudulent transactions, unauthorised charges, and billing errors go unnoticed for months when customers do not check their statements regularly. Make it a habit to review your account at least once a week, whether through the app or online banking portal.

Borrowing Without Comparing Options

Many customers take loans from their existing bank without comparing rates elsewhere. Loyalty does not always mean better pricing. Before accepting any loan or mortgage offer, compare rates from at least three different lenders. The difference can amount to thousands over the life of a loan.

Underusing Digital Banking Features

Traditional banks now offer reasonably capable online and mobile banking tools that most customers never fully explore. Automatic savings transfers, bill payment schedulers, spending alerts, and account statements are all available and all free. Using them costs nothing but a few minutes of setup and saves real money and stress over time.

Not Having an Emergency Fund

One of the most important things a traditional bank account can do for you is hold an emergency fund. Many beginners make this mistake: they spend their full monthly income and leave nothing in reserve. Financial advisors consistently recommend keeping three to six months of living expenses in an accessible savings account. A traditional bank savings product is a natural home for this fund.

Conclusion

Traditional banking has survived for centuries because it solves real problems. It keeps money safe, moves wealth between people and institutions, funds the purchases and businesses that drive economies, and provides a stable financial foundation for individuals and families.

Its limitations are real. Fees can be high, processes can be slow, and digital experiences often fall short of what modern customers expect. But these are problems that good traditional banks are actively working to solve, and they do not erase the genuine strengths of a regulated, full-service financial institution.

The future of banking is not purely traditional and not purely digital. It is a hybrid. The best financial consumers in the coming decade will be those who understand both systems well enough to use each one where it genuinely excels.

Use your traditional bank for what it does best: security, lending, complex financial products, and cash access. Use digital tools for what they do best: speed, transparency, budgeting, and everyday money management. Build strong habits around both, and your financial life will be better for it.

Banking is not just a system you interact with. It is a tool you can use to build the financial future you want. The more clearly you understand how it works, the better you can make it work for you.

Frequently Asked Questions

Q: What is traditional banking?

Traditional banking refers to the financial services offered by licensed, regulated banks through a combination of physical branches and digital channels. These services include current and savings accounts, loans, mortgages, credit cards, and financial advice. Traditional banks are regulated by government authorities and covered by deposit protection schemes.

Q: How does traditional banking work?

Traditional banks collect deposits from customers, pay interest on those deposits, and lend the money to borrowers at a higher interest rate. The difference between the interest paid to depositors and the interest earned on loans is the bank's primary source of income. Banks also earn fees from account services, card products, and financial advice.

Q: Is traditional banking safe?

Yes, for most customers in regulated markets. Traditional banks operate under strict government oversight. Deposits are typically insured up to a set limit by a national deposit protection scheme. While no financial institution is completely risk-free, the regulatory framework around traditional banking is designed to protect depositors and maintain stability.

Q: What are the main advantages of traditional banking over digital banking?

Traditional banking offers physical branch access, cash handling services, in-person financial advice, a full range of complex financial products, including mortgages and business loans, and a long track record of regulatory compliance. It suits customers who value personal relationships with their bank, need help with complex financial decisions, or regularly handle cash.

Q: How do beginners get started with traditional banking?

Start by researching the banks available in your area and comparing their account options and fee structures. Visit a branch or apply online for a basic current account. Bring your identity documents and proof of address. Once your account is open, set up online banking access, explore the available savings products, and start building a healthy banking relationship by keeping your account in good standing.

Q: Should I use a traditional bank or a digital bank?

The most practical answer for most people is to use both. Keep your primary accounts, savings, and any credit products with a traditional bank for security and access to complex financial products. Use a digital banking app for everyday spending and money management. This combination gives you the strengths of both systems without being limited by the weaknesses of either.

Share this article

Related Articles

10 Best Fintech Companies in the UK You Must Know

Discover the 10 best fintech companies in the UK for banking, payments, lending, and business finance. Compare Revolut, Wise, Monzo, Starling, and more to choose the right fintech solution.

Top 20 Fintech Companies in the USA Leading Financial Innovation

Discover the 20 best fintech companies in the USA transforming banking, payments, investing, and lending. Compare top innovators to find the right financial technology solution.

Digital Banking Explained: A Complete Guide to Online Banking, Mobile Finance, and Smarter Money Management

Discover digital banking in 2026 with online banking, mobile finance apps, secure payments, and smart tools that make managing money easier, faster, and safer.