Finance Monitoring Guide: How to Track, Manage, and Take Control of Your Money

Take control of your finances with this complete finance monitoring guide. Learn how to track spending, manage budgets, monitor savings, and make smarter money decisions in 2026.

At the end of the month, most people feel like their money simply disappeared. They paid the bills, bought groceries, ate out a few times, and somehow the account is far lower than expected. They have a rough idea of what happened, but no clear picture.

That is the problem finance monitoring solves. It gives you an exact, real-time view of where every pound or dollar goes, what patterns are costing you the most, and what changes would make the biggest difference to your financial health.

This guide explains what finance monitoring is, how it works, which tools make it practical, and how to build a simple daily and weekly routine that keeps you genuinely in control of your money without spending hours on spreadsheets.

What is Finance Monitoring?

Finance monitoring is the ongoing process of tracking, reviewing, and understanding your personal or business financial activity. It covers everything that moves through your accounts: money coming in (income), money going out (expenses), what you save, what you owe, and how your financial position changes over time.

It is not the same as budgeting. Budgeting is planning how you will use your money. Financial monitoring is checking whether reality matches that plan and adjusting when it does not. The two work together, but monitoring is what keeps budgeting honest.

Why finance monitoring matters today

Most spending happens automatically, subscriptions, direct debits, and card payments go out without a second thought. Without monitoring, these costs accumulate invisibly.

Small daily purchases add up to large monthly totals that most people significantly underestimate without data.

Financial goals without tracking are just wishes. Monitoring turns them into measurable progress with a clear timeline.

Alerts and dashboards catch problems, such as overspending, unusual charges, or missed savings targets, before they become serious issues.

Understanding your cash flow puts you in control of financial decisions rather than reacting to surprises at the end of the month.

How Finance Monitoring Works

Financial monitoring works by collecting your financial data, organising it into categories, and presenting it in a way that shows clear patterns and gaps. Here is how the process breaks down.

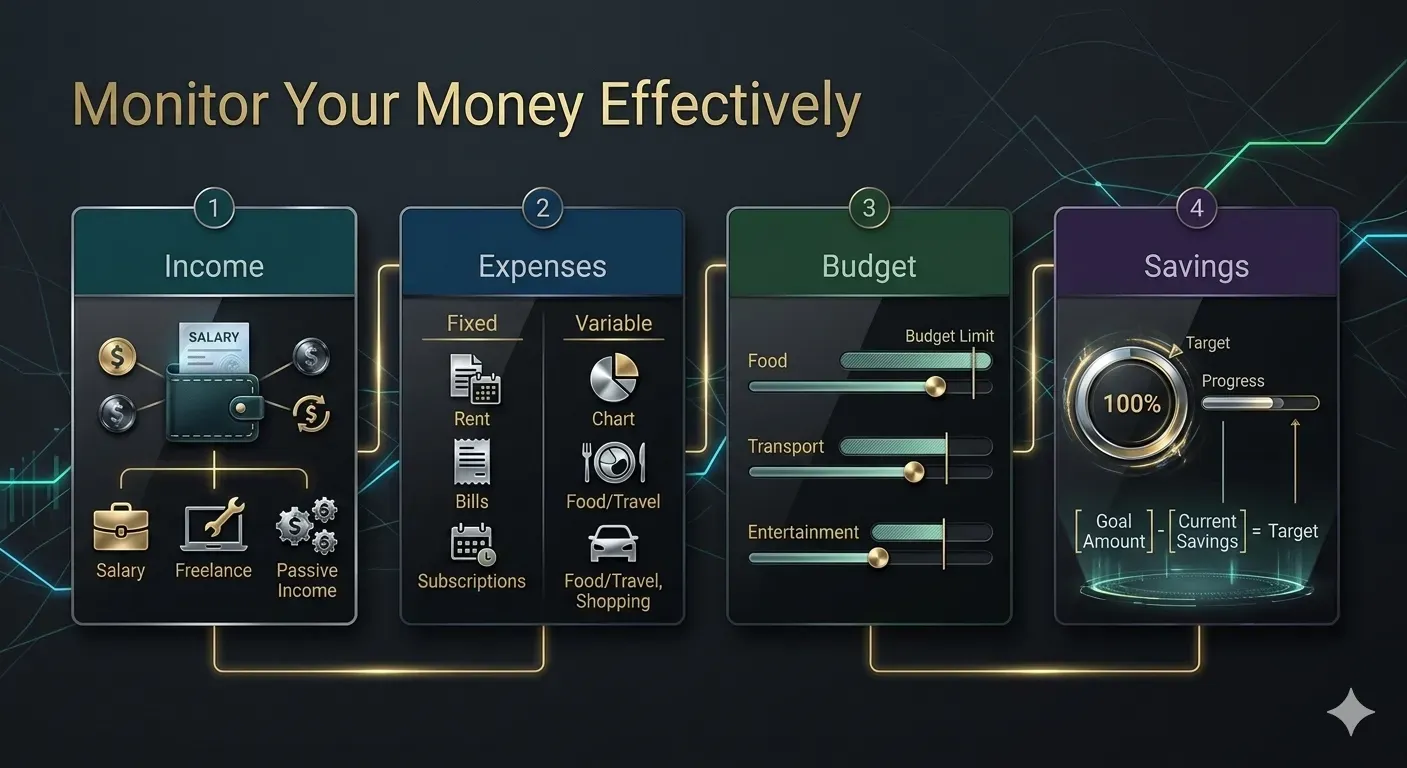

The five core categories

Categor | What it covers | Why it matters |

|---|---|---|

Income tracking | Salary, freelance payments, rental income, side earnings | Confirms what actually arrived vs. what was expected |

Expense tracking | Every payment out: bills, food, transport, subscriptions | Identifies where money goes and which categories are over-budget |

Budget monitoring | Comparing planned spend to actual spend by category | Shows the gap between intention and reality |

Savings tracking | Progress toward savings goals and emergency funds | Keeps long-term goals visible and measurable |

Alerts and reports | Notifications when limits are hit; monthly summaries | Catches problems early before they compound |

Manual tracking vs. automated tools

Manual tracking means entering your transactions yourself in a spreadsheet, notebook, or basic app. It gives you full control and costs nothing. The problem is consistency. In real life, most users struggle to keep manual records up to date for more than a few weeks before the habit slips.

Automated finance monitoring tools connect to your bank account and import transactions automatically, categorise them using AI, and update your dashboard in real time. You spend minutes reviewing instead of hours entering data.

Approach | Effort require | Accuracy | Best for |

|---|---|---|---|

Manual spreadsheet | High: daily data entry | Depends on consistency | People who prefer full control |

Manual finance app | Medium: some entry needed | Good if maintained | Beginners building the habit |

Automated tool | Low: review only | High: auto-imported | Most users want reliable data |

Automated + dashboard | Very low | Very high | Busy users tracking multiple goals |

Finance Monitoring Tools: How They Work and How to Use Them

Finance monitoring tools range from simple expense trackers to comprehensive financial dashboards. What they all share is the ability to turn raw transaction data into clear, actionable summaries.

What good finance monitoring tools do

Import transactions automatically from connected bank accounts and credit cards

Categorise spending: food, transport, entertainment, and bills without manual sorting.

Compare your actual spending to your planned budget in real time

Track progress toward savings goals and show your current timeline

Send alerts when you approach or exceed category limits

Generate monthly reports showing spending trends over time

How to start using a finance monitoring tool

Connect your bank account or import your recent bank statements. Most tools offer secure open banking connections that sync automatically.

Review the automatic categories. Correct any miscategorised transactions: for example, a supermarket trip categorised as entertainment.

Set your budget limits for each spending category based on your income and financial goals.

Enable spending alerts so the tool notifies you when you are approaching a budget limit in any category.

Set at least one savings goal: amount, timeline, and monthly contribution needed, so that the tool can track your progress.

Review your dashboard weekly and your monthly report at the end of each month. Adjust budgets based on what you learn.

The Real Benefits of Finance Monitoring

The practical case for monitoring your finances is straightforward: you cannot manage what you cannot measure. Here are the concrete benefits of regular monitoring.

1. Better budgeting through real data

Most people build budgets based on estimates and good intentions. Finance monitoring replaces estimates with facts. After one month of tracking, you know exactly what you actually spend on food, transport, and entertainment, not what you think you spend. That data makes your next budget far more accurate and realistic.

2. Significantly lower overspending

Awareness alone reduces overspending. When people know their spending is being tracked and can see it in real time, impulse decisions decrease. Seeing that you have already spent 80% of your monthly entertainment budget on the 15th of the month changes how you approach the remaining two weeks.

3. Faster progress toward savings goals

Finance monitoring makes savings goals visible daily rather than vague aspirations reviewed once a year. When you see your emergency fund grow from £1,400 to £1,650 over the month, motivation stays high. When the tracker shows you are £200 behind your goal, you have a clear target to close the gap.

4. Smarter, faster financial decisions

When you have a clear financial dashboard, decisions become easier and more confident. Can you afford a weekend trip? Check your surplus. Should you upgrade your phone? Check your savings timeline. Should you cut a subscription? Check whether you actually used it. Data replaces guesswork.

How to Monitor Your Money Effectively

Effective finance monitoring is not about checking your balance obsessively. It is about having a structured system that gives you the right information at the right time, without consuming hours of your week.

Know your income baseline

Start with total monthly income from all sources. Include salary, freelance income, rental income, and any regular transfers. This is your starting number; everything else is measured against it.

Fixed income (same every month): easy to plan around

Variable income (freelance, commission): use your three-month average as your planning baseline

Multiple income sources: track each separately so you can see which are growing or declining

Separate fixed from variable expenses

Fixed expenses are predictable: rent, loan repayments, insurance and subscriptions. Variable expenses change each month: food, transport, entertainment and clothing.

Fixed expenses are harder to change quickly, but easy to forecast

Variable expenses are where monitoring delivers the most impact, small behavioural changes here compound significantly over months

Review your fixed expenses quarterly to catch subscriptions you are no longer using

Set category spending limits

Based on your income and fixed costs, assign a realistic monthly limit to each variable category. Use your actual data from the previous month as the starting point, then adjust toward your target.

Track progress toward savings goals

Every savings goal needs three numbers: a target amount, a deadline, and a monthly contribution needed to reach it. Finance monitoring tools calculate this automatically and show your current progress as a percentage.

Monthly savings needed = (Goal amount − Current savings) ÷ Months remaining Example: Goal: £5,000 | Current savings: £1,200 | Months remaining: 8 Monthly needed: (£5,000 − £1,200) ÷ 8 = £475/month |

How Finance Monitoring Apps Work

Finance monitoring apps are the practical tools that make the system described above work automatically. Understanding how they operate helps you use them more confidently and get better results.

The core logic behind finance apps

Remaining balance = Total income − Total expenses Budget status = Category limit − Actual spending in category Savings rate (%) = (Monthly savings ÷ Monthly income) × 100 Goal progress (%) = (Current savings ÷ Goal amount) × 100 Months to goal = (Goal − Current savings) ÷ Monthly contribution |

The Best Strategy: Combining Budgeting, Tracking, and Saving

Finance monitoring works best when it connects three systems: a budget (your plan), a tracker (your reality check), and a savings structure (your forward progress). Each one reinforces the others.

A practical daily and weekly routine

Daily (2 minutes): Glance at your finance dashboard. Check your remaining balance and whether any categories are close to their limits. No analysis needed, just awareness.

Weekly (10 minutes): Review the week’s transactions. Correct any miscategorised items. Check your savings goal progress. Note any category that appears likely to overshoot at the end of the month.

Monthly (20–30 minutes): Read your monthly report. Compare actual vs budgeted for every category. Adjust next month’s budgets based on what you learned. Update savings goal timelines if your situation has changed.

Quarterly (30–45 minutes): Review all fixed expenses and subscriptions. Cancel anything you are not actively using. Reassess your savings goals. Are they still the right targets? Do the amounts still make sense for your current income?

The three-tool setup that works for most people

One mobile banking app for real-time balance and transaction history

One budgeting and monitoring tool for category tracking, alerts, and monthly reports

One savings goal tracker (often built into the budgeting tool) for progress visibility

Common Finance Monitoring Mistakes to Avoid

1. Ignoring small expenses

A £4.50 daily coffee, a £9.99 subscription, a £7 impulse purchase- none of these feels significant individually. Together, they can represent £150–200 per month in untracked spending. Finance monitoring shows these patterns clearly. The habit of tracking small purchases often matters more than any single large decision.

2. Skipping the monthly review

Many beginners make this mistake: they set up tracking but never review the monthly report. The report is where the value actually lives. Weekly check-ins keep you on track day-to-day, but the monthly review is where patterns emerge, and real financial decisions get made. Schedule it as a fixed calendar event.

3. Weak or unrealistic budgeting habits

Setting a £150 food budget when you consistently spend £280 does not create discipline; it creates frustration and then abandonment. Use your actual monitoring data to set budgets that reflect reality first, then reduce them gradually toward your target. Incremental improvement sustained over months beats ambitious targets abandoned in weeks.

4. Not setting specific financial goals

From a practical perspective, finance monitoring without a goal is just data collection. The power comes from connecting your tracking to a target: a specific savings amount, a debt payoff date, a holiday fund total, or an investment contribution. Goals give your monitoring purpose and keep the habit alive through months when motivation is low.

5. Inconsistency in reviewing and updating

Finance monitoring is a habit, not a one-time setup. The users who benefit most are the ones who check their dashboard regularly and update their budgets as their lives change after a pay rise, a new expense, or a financial goal reached. Inconsistent monitoring produces incomplete data and unreliable insights.

Conclusion

Finance monitoring is not about restriction or stress. It is about clarity. When you know exactly where your money goes, you make better decisions, reach goals faster, and stop being surprised at the end of every month.

Here is what to carry forward from this guide:

Finance monitoring is the process of tracking income, expenses, savings, and cash flow in real time, connecting your plan to reality

Automated tools make monitoring practical by importing transactions, categorising spending, and generating monthly reports without manual data entry.

The five core categories: income, expenses, budgets, savings, and alerts give you a complete financial dashboard.

Effective monitoring requires a consistent routine: daily awareness, weekly review, monthly analysis, and quarterly goal check-ins.

Common mistakes: ignoring small expenses, skipping monthly reviews and setting unrealistic budgets are all avoidable with a structured approach

Start simple: one tool, one month of data, and one category to improve. Build from there.

Frequently Asked Questions

Q: What is finance monitoring?

Finance monitoring is the ongoing process of tracking and reviewing your financial activity: income, expenses, savings, and cash flow to stay informed about where your money goes and whether you are on track toward your financial goals. It combines real-time transaction tracking, category budgeting, spending alerts, and monthly reporting into a system that keeps your financial decisions grounded in accurate data rather than estimates.

Q: How can I monitor my finances?

You can monitor your finances manually using a spreadsheet or notebook, or automatically using a finance monitoring app that connects to your bank account and imports transactions in real time. The most effective approach is to use an automated tool for transaction tracking, set category spending limits, enable alerts when you approach those limits, and review a monthly report to identify patterns and adjust your budget. The key is consistency, weekly check-ins, and monthly reviews deliver far more value than occasional use.

Q: What are the best finance monitoring tools?

The best finance monitoring tool for you depends on your needs and situation. For beginners, a mobile app that automatically categorises transactions and shows a simple spending dashboard is the right starting point. For users managing multiple goals or irregular income, a tool with customizable budgets, goal trackers, and detailed monthly reports adds more value. Look for tools that offer bank-grade security, support open banking connections, and provide alert features. Most good tools offer a free tier sufficient for individual personal finance monitoring.

Q: Is financial monitoring important?

Yes, consistently. Research and real-world experience both show that people who actively monitor their finances save more, carry less unnecessary debt, and make more confident financial decisions than those who manage money reactively. The act of monitoring creates awareness, and awareness changes behaviour. Small improvements in spending habits, maintained consistently over months, produce significantly better financial outcomes than occasional large financial decisions made without data.

Q: How do beginners start tracking money?

The most effective starting point for a beginner is to choose one simple finance monitoring app, connect it to your primary bank account, and spend the first week reviewing the automatic transaction categories without trying to change anything. After one full month of data, you will have an accurate picture of your actual spending patterns. From there, set one or two budget limits in the categories where your spending surprised you most. Add a savings goal. Review weekly for five minutes. Build the habit before adding complexity.

Share this article

Related Articles

10 Best Fintech Companies in the UK You Must Know

Discover the 10 best fintech companies in the UK for banking, payments, lending, and business finance. Compare Revolut, Wise, Monzo, Starling, and more to choose the right fintech solution.

Top 20 Fintech Companies in the USA Leading Financial Innovation

Discover the 20 best fintech companies in the USA transforming banking, payments, investing, and lending. Compare top innovators to find the right financial technology solution.

Digital Banking Explained: A Complete Guide to Online Banking, Mobile Finance, and Smarter Money Management

Discover digital banking in 2026 with online banking, mobile finance apps, secure payments, and smart tools that make managing money easier, faster, and safer.